It is safe to say it has been an energetic start to the year, underscoring meaningful shifts in the economic landscape and rate expectations.

Last week delivered a busy slate of tier-1 risk events; this week’s economic calendar, however, offers a lighter docket. Monday is poised to be a snooze. Void of tier-1 numbers and US banks closing in observance of Presidents’ Day, volatility is likely to slow heading into US trading hours.

RBA minutes

The Reserve Bank of Australia (RBA) minutes will be released on Tuesday at 12:30 am GMT and could be one worth observing for Asia Pac traders, though it is doubtful we’ll see much more than what we already know.

You may recall that the central bank left the Cash Rate unchanged at 4.35% at its first policy-setting meeting this year, a 12-year high. In addition, the accompanying Rate Statement pencilled in a fresh line noting that further policy tightening ‘cannot be ruled out’. However, on the other side of the fence, according to the Statement of Monetary Policy (SoMP), the central bank’s projections announced a downward revision to its growth and inflation forecast, alongside higher unemployment. The RBA anticipates CPI inflation (as well as trimmed-mean inflation) to cool to 2.8% by the end of 2025 (November’s forecast: 2.9%) and (for CPI inflation) to slow to 3.2% at the end of 2024 (November’s forecast: 3.5%). Unemployment will peak at 4.4% in mid-2025 and hold at this level until the year-end, with GDP growth expected to be at 2.1% in mid-2025 (down from November’s 2.2% reading).

Fed minutes

The minutes from the latest FOMC rate decision will be on the watchlists for many this week on Wednesday at 7:00 pm GMT.

Last week’s hotter-than-expected US CPI data (inflation continues to cool but not as fast as we expected) reinforced the dollar and witnessed an unwind in Fed rate-cut pricing, consequently bringing market expectations more in line with the Fed. In the latest SEP, you may remember that the Fed projects only three rate cuts this year. Hence, we head into the minutes with not only elevated inflationary pressures but also resilient economic GDP growth and a tight labour market. As a result, the recent dovish repricing should not raise too many eyebrows. According to the futures market, the first 25bp rate cut is now priced out to June (March is all but a sealed deal for another no-change with only a 10% probability of a 25bp cut), with 93bps of easing forecast for the year ahead (just shy of four rate cuts).

The last Fed policy meeting at the end of January revealed a language change in the Rate Statement, striking a line through a familiar sentence that referenced the central bank’s readiness to increase rates: ‘… additional policy firming that may be appropriate to return inflation to 2 percent over time’. While dropping this sentence suggests a dovish shift, the substitute delivered a hawkish vibe to the proceedings, signifying that the central bank is not rushing to cut rates until inflation has further softened.

Ultimately, another pushback against a March cut could be seen in the minutes, which would be logical at this point and may bolster demand for the dollar in the short term. With that being said, in the event of a lack of any fresh insights from the minutes (the most likely course), the report might be difficult to trade with any conviction.

February PMIs

Thursday will see the release of PMIs from the eurozone (9:00 am GMT), the UK (9:30 am) and the US (2:45 pm).

In the UK, last week directed the spotlight to a slew of tier-1 economic numbers, including wages, which came in higher than expected, as well as CPI inflation and GDP data revealing larger-than-expected misses which weighed on sterling (MTD, GBP is down -0.7% against the US dollar). The latest GDP data also elbowed the UK into a mild technical recession (to be frank, the UK economy [as well as the euro zone] has been stagnating for several quarters). The week wrapped up with retail sales rebounding across the board in January.

Therefore, this week’s UK business surveys will be widely monitored. On the service side of the PMIs, we entered expansionary territory in late 2023 after a pickup. Manufacturing, however, remains in contractionary territory, though less so than it was in mid-2023: contracting at a slower pace. Market consensus as of writing is for the services PMI to tick slightly higher to 54.4 in February from January’s 54.3, while the manufacturing PMI is forecast to rise to 47.5 in February from 47.0 in January. As most are aware, the PMIs can move the market’s needle quite significantly if out-of-consensus prints are observed. Following the CPI and GDP miss and given sterling failed to rally beyond the $1.26 handle on Friday on the back of the UK retail sales beat (data surpassed estimate range highs on headline and ex-fuel components), a miss on the PMI data this week could help the pound breakout beyond stubborn range lows of $1.2540. A stronger-than-expected release, nevertheless, may prompt hawkish repricing, nudging rate expectations further out in the year for the first 25bp cut and ultimately underpinning sterling from range support.

OIS pricing forecasts that the Bank of England (BoE) will cut rates by 25bps at August’s policy-setting meeting and, in total, ease by 72bps (or three rate cuts) by the end of the year, showing that markets expect that the BoE will be one of the last major central banks to begin easing (the Fed is expected to step up in June, as highlighted above, while the ECB are expecting to cut in Q2). This reflects quite the change from the beginning of the year when markets were pricing in around five rate cuts!

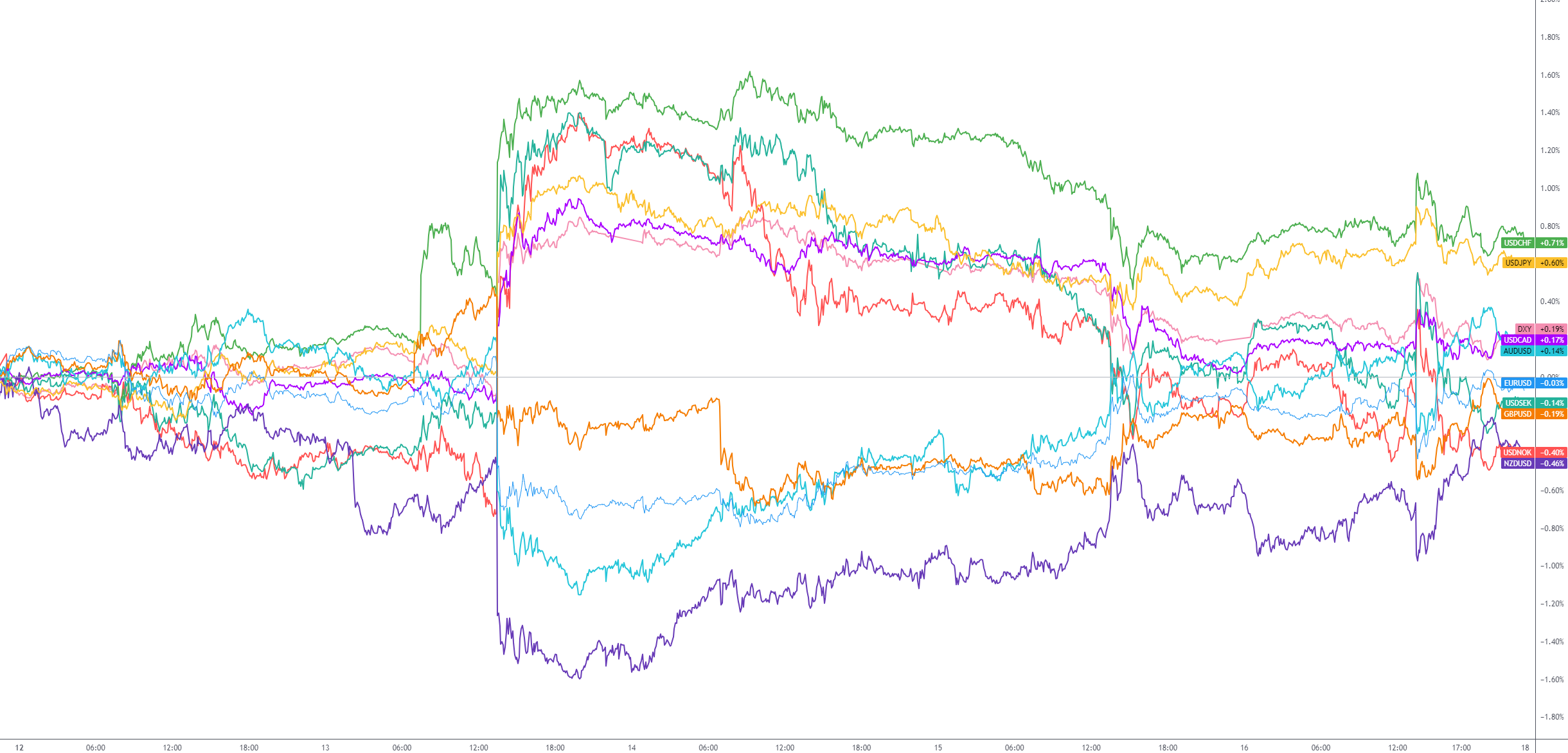

G10 FX (five-day change):

previous

previous